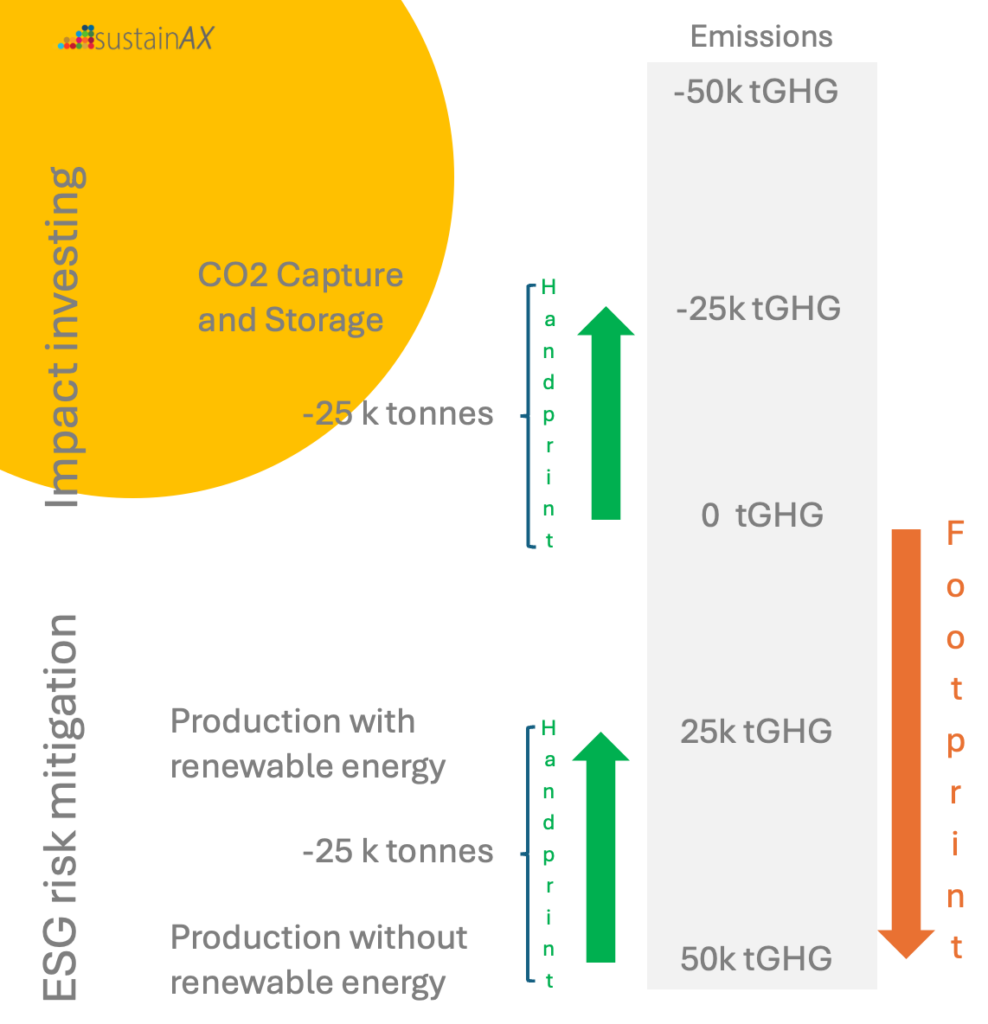

Of course, this is stylistic to simplify, even impact strategies must do ESG risk integration and very often they also practice engagement with companies to make them mitigate ESG risks as all activities have some “footprint”. No doubt it can be a little blurry and the difference in intention can easily be forgotten.

What works – Corporates will only move when risk adjusted returns are under threat or can improve

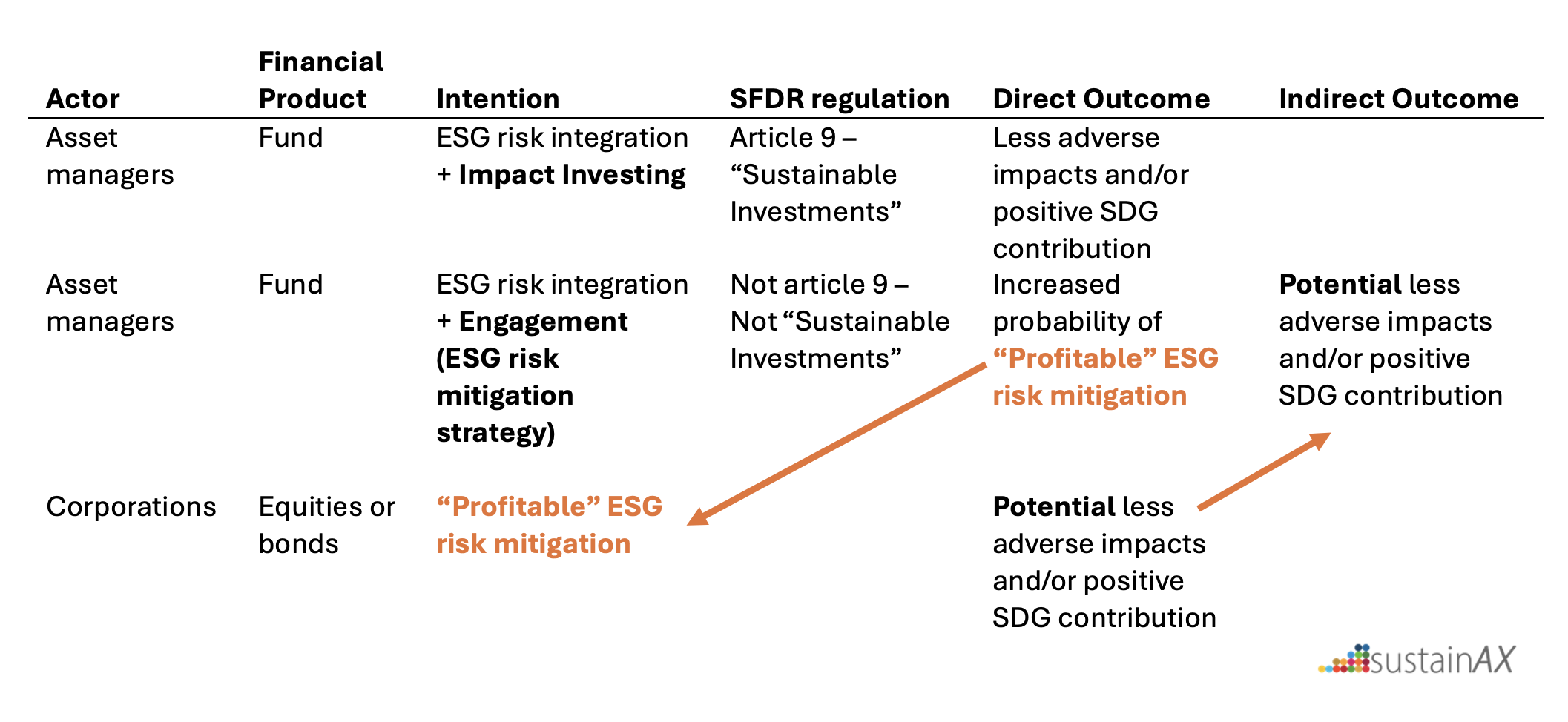

Only corporates can do “real” ESG risk mitigation and only ESG risk mitigation where the cost of the risk mitigation is less than the gain (higher revenue, lower costs, lower risks) will be addressed for most of them as this is what the board and management is limited to do according to the corporate statutes combined with the directors’ fiduciary duty (including duty of loyalty and duty of care). We can call this “profitable” ESG risk mitigation.

Therefore, the better companies understand their ESG risks, the more “profitable” ESG risk mitigation can be, as for most companies the ESG risk is probably higher than understood. ESG risk research plays a crucial role to the difference of sustainability reporting here as the ESG risk level must be assessed and understood before companies will react.

Conclusion

Not only impact investing has positive impact on environmental and social goals, ESG risk mitigation strategies can also have positive impact.

On one hand, companies’ board of directors or C-suite members do not have the permission to spend company resources on a program that is not intended to increase sales, reduce costs, or reduce risk unless explicitly stated in the company statuses. Therefore, calling out companies asking for anthropology, or “unprofitable” ESG risk mitigation is not productive. It is waste of time.

On the other hand, “profitable” ESG risk mitigation is something companies do understand, and it is within their mandate. Therefore, focus should be on helping companies understand the full environmental and social cost of their activities and the resulting ESG risk aspects, and here investors have a role to play through engagement. This will lead to ESG risk mitigation with, in many cases, positive impacts on the environmental and social goals, like the SDGs, but only as an unintended side-effect. Companies and investors should be transparent about the latter!

Table 1 – How impact investing and ESG risk mitigation (Engagement) strategies can meet in Outcomes despite very different Intentions

Global assets under management with ESG risk integration is massive compared to impact strategies, therefore engagement leading to ESG risk mitigation have more total absolute impact than impact investing! An assumption here is that proper ESG risk integration processes are in place and well executed, this is likely not yet the case globally, but will be.