THE INEVITABLE ESG RISK ASCENDANCE – Asset Valuation and Insiders

In the raging debate on LinkedIn between impact seekers and ESG risk mitigators, amid the aggressive criticism of ESG risk rating providers and EU Sustainable Finance regulation, and complaints of lacking progress on mitigation of Principal Adverse Impacts like GHG emissions, we see a theme growing out of all this noise; the INEVITABLE ASCENDANCE of ESG risk through increasing practice of “modern” ESG risk integration in investment decisions. Be sure you understand this if you care about maximising expected risk adjusted returns.

ESG risks

First, what are ESG risks? In the EU Sustainable Finance regulation this is defined as Sustainability risk and includes Environmental, Social and Governance risks. It is not new for portfolio managers and analysts, but both the depth and the width have increased over time. For an ESG risk analyst, ESG risks includes opportunities, the scale goes from positive to negative.

ESG risk integration

Second, what is ESG risk integration? ESG risk integration is the action to integrate ESG risks in the investment processes, that in practice means investment decisions. To be able to do this, the ESG risks must be fully understood in the first place. This requires internal or external ESG risk research and cannot be read out of an ESG rating or score. Thereafter, the identified ESG risks should be transformed to financial metrics, potentially leading to adjustments of profit & loss or balance sheet elements that in their turn again will impact valuation of assets. It can as an alternative lead to adjustments of required risk premiums and equivalent for bond investments.

ESG risk integration – Status 2023

Despite all nice text on many asset managers’ websites about ESG risk integration, stemming from requirements of the article 6 in SFDR (EU Sustainable Finance Disclosure Regulation) that was implemented less then 3 years ago in 2021 in the EU, the real processes of ESG risk integration are often very weak if existing at all. There can be a large gap between what is communicated and what really happens.

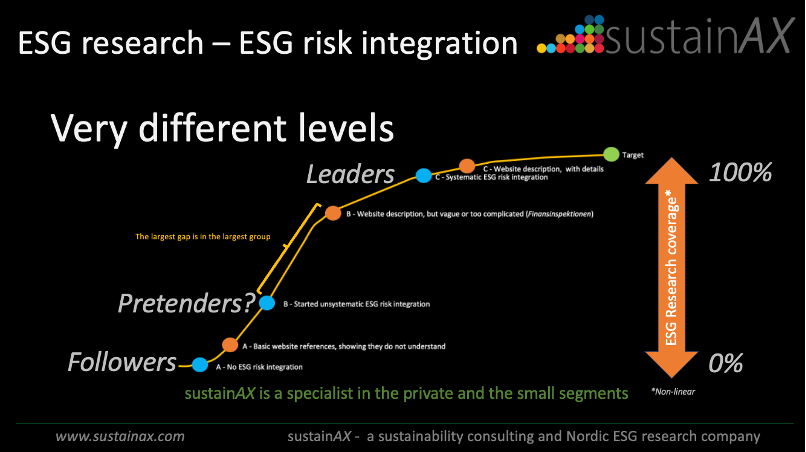

Figure 1 – Difference in communicated and practiced ESG risk integration

Source: sustainAX, October 2023. Groups A, B and C, and the gap between their web disclosure and their practice of ESG risk integration.

One reason can be that there is no full understanding of the ESG risks. For instance, the “old” way of approaching this is to mainly focus on existing controversies and corporate governance issues. Another reason can be that the work to translate the identified ESG risks to financial metrics is too difficult or too demanding and therefore does not happen. There is with other words a gap between description and reality, but unlike the map and terrain where this is a normal expected characteristic, this gap is a problem that need to be addressed, but not only because the information given does not reflect reality and is false marketing. The INEVITABLE ASCENDANCE of ESG risk is another reason.

THE MAIN POINT: The ESG risk ASCENDANCE

Today, we have a much better understanding of ESG risks of a company due to historic and ongoing development of the ESG risk area plus a growing global specialist community. This is today mainly driven by climate and nature changes and stakeholder activism, leading to stakeholder reactions. It is a domain for specialists, the practising ESG risk analysts. It can be catastrophic for companies and investors to ignore this.

As the practice of real “modern” ESG risk integration is still in its infancy, it does not yet have an important impact on asset pricing at large. For sure, some fossil fuel related assets see discounts and large deficiencies or controversies have impact, but it is still not having a noticeable impact on asset pricing across all sectors and across all relevant ESG risks.

What is likely to happen as the asset managers really start to implement fully “modern” ESG risk integration is that it will have a heavier weight in the valuation of assets. And this is not an area where the followers will be the winners. Many smaller asset managers have chosen a clear follower strategy in the ESG field up until now.

A follower strategy in this area is leading to misjudgement of the risks that the market will to an increasing extent price in going forward. That said, in the short run this may also be the case for leaders in the area, but in the longer run they will be winners. There is no symmetry here as time drives us closer and closer to the moment in time when the leaders will be right.

Side effect: Insider information in engagement meetings?

A side effect of this is that information given by companies to investors on a private basis in an engagement meeting may be considered insider information in the future. Information that is considered not having an impact on asset pricing is not considered insider information, but with growing ESG risk integration practice, the impact on asset valuation increases and the information given can be considered differently and should be treated like financial information. This is not a discussed theme in the market today but it is time to pick it up!

Conclusion

Do not miss out on this growing component of asset valuation on a wider scale. It is therefore crucial to get correct ESG risk integration processes going. It may be painful at the beginning as it requires additional work for the same pay, but it is strategically important for an asset manager to deal with this properly now.

How to get there? First, ensure ESG risks are fully understood for investment objects by ensuring you have access to ESG risk research, internal or external. Second, get the “modern” ESG risk integration processes going by training the portfolio managers and analysts in ESG risk integration.

Where are you in this dimension? Let us know what you think!