ESG* reporting – Is sustainability reporting running away from your sustainability strategy and ESG score?

With over 120 company ESG research reports and ESG scores made available to our clients, we see trends in sustainability reporting, for the good and the bad. As we are specialists in ESG research of the smaller companies and private companies, we see many of them in early phases of their sustainability journey. We also see how they are developing over time.

In this article, we’ll show you the different typical stages of a company’s sustainability reporting. We will comment these and try to reason around them. Furthermore, we’ll lean into the map and landscape aspect with regards to ESG scores and the regulatory impact on the focus in the area. Finally, some recommendations to the companies working on their sustainability strategy.

Trends that at times we find worrisome for corporate sustainability reporting

Let us agree on one point, it is great that companies report on their sustainability work and status. The reporting can be qualified on different dimensions, of which we see clearly the three most important are:

- The sustainability reporting volume

- The sustainability reporting quality

- The sustainability reporting’s reflection of a real sustainability strategy

Interestingly, these three aspects do not at all move in tandem as we would like them to do based on the principle that you should not claim what you do not really do…

Let’s graph this and then thereafter discuss the phases and try to explain why it is like this.

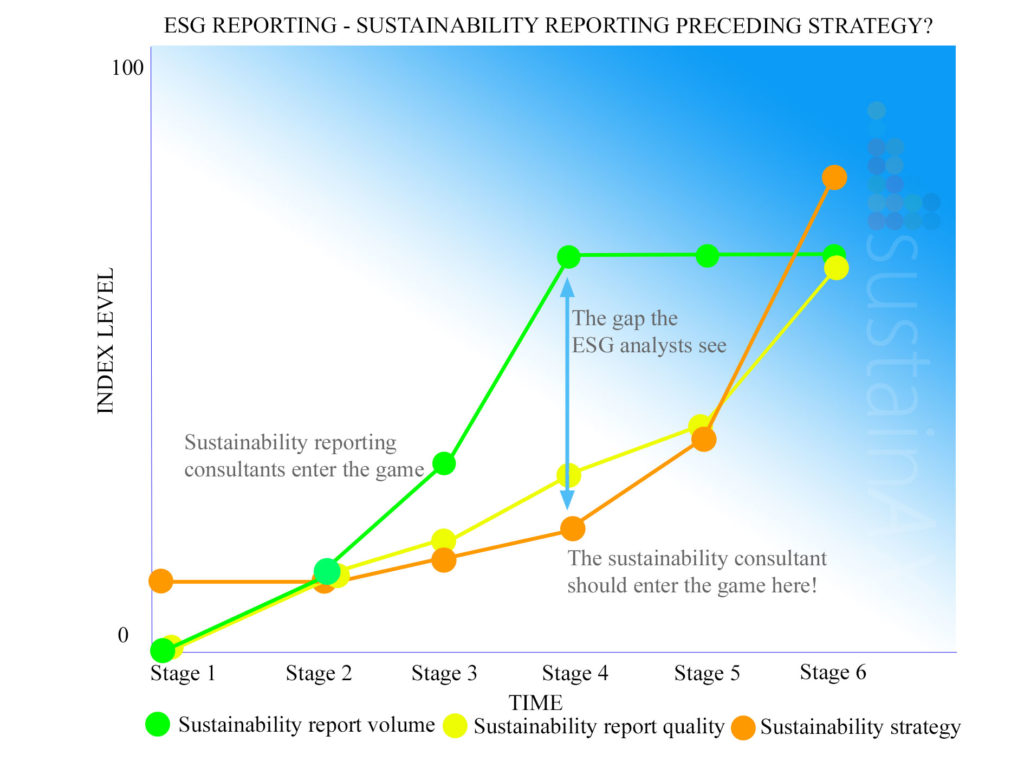

GRAPH 1 – The different phases of the different dimensions of corporate sustainability reporting

Source: sustainAX, November 2021

Stage 1

The company is doing the right things with H&S, code of conduct policies, take some environmental considerations in their operations and talk about good business practice with their partners. Corporate governance is simple.

But they do no sustainability reporting at all – and yes, I confirm we see these companies still in our universe.

The result is a high ESG risk as we do not know how they address their ESG risk exposure when seen from the outside

Stage 2

The company starts to get questions on sustainability from their stakeholders and initiate simple sustainability reporting that tell what they have in place and what they do. Nothing more, nothing less. Some low hanging KPI fruits are added. Most start on the governance side, where most investors are comfortable to address issues. Other examples can be outlining policies in place and maybe sick leave KPIs.

The result is a little lower ESG risk versus stage 1 as we still do not know how they address all ESG risks when seen from the outside

Stage 3

Whoa, what happened? All of a sudden, we see 4-5 pages or more of pure sustainability reporting. But it is mostly consisting of more words and often repeated many times throughout their website and annual report. Not many more clear action descriptions or KPIs, just more words, creating a collection of narratives that long to be strengthened with hard information, KPIs. Maybe someone in the company took a sustainability reporting class or maybe did they hire new knowledge? Notice the lagging reporting quality and sustainability strategy link. What if the company worked on the sustainability strategy before the sustainability reporting? The latter point is easier for a certified ESG analyst to see, for a non-trained eye the good-looking sustainability report is doing well in a tick off exercise; «Is the company good on sustainability», «Yes»; check!

The result is a little lower ESG risk versus stage 2, but here the non ESG specialist, with low ESG knowledge, tend to not agree with our “too small” improvement in ESG score

Stage 4

Now we are leapfrogging, this is where the CSR consultants come in, as the company wish to accelerate on sustainability reporting. It really looks nice, and all the sustainability terms are correct, and the structure of the sustainability reporting is as it should be, logic and easy to follow. Some more KPIs are added, even some with history, and it is nice to see Scope1, 2 and 3 show up as well, even if the Scope 3 only englobe the air travel of the employees. But notice that even if the reporting quality and sustainability strategy link are improving, they still lag a lot. But it starts to hurt, investors are asking all these detailed questions they cannot find in the glossy sustainability report and the company need to define real action plans behind the allusion to such as the narratives have made. Stakeholders also ask for more KPIs as justification of what the company claims. The topic is defined on the Board of Director level and the management is asked to develop further the sustainability strategy. Finally, some deeper processes get going!

The result is a tad lower ESG risk versus stage 3, but here the non ESG specialist, with low ESG knowledge, tend to not agree with our “too small” improvement in ESG score

Stage 5 and 6

Thanks, the fact that it ended up in a heated discussion in the Board of Directors in the previous stadium (around resources, costs and strategy) led to a lot of real changes. Policies were redefined and more precise, compulsory training of the personnel was installed and KPIs are reported. Action plans on all material E and S areas are defined with relevant KPIs that will be frequently reported on. And all of this is now used in first place as internal management tools and thereafter reported in the sustainability report. So instead of being «just» reporting it is now understood to be a real management tool. With other words, the company is focussing on becoming more sustainable instead of “only” focussing on reporting about it. The company’s sustainability strategy is at this stage catching up with the sustainability reporting. Finally!

Now the ESG score can improve a lot versus stage 4 if the sustainability strategy is relevant and credible, and well reflected in the sustainability reporting

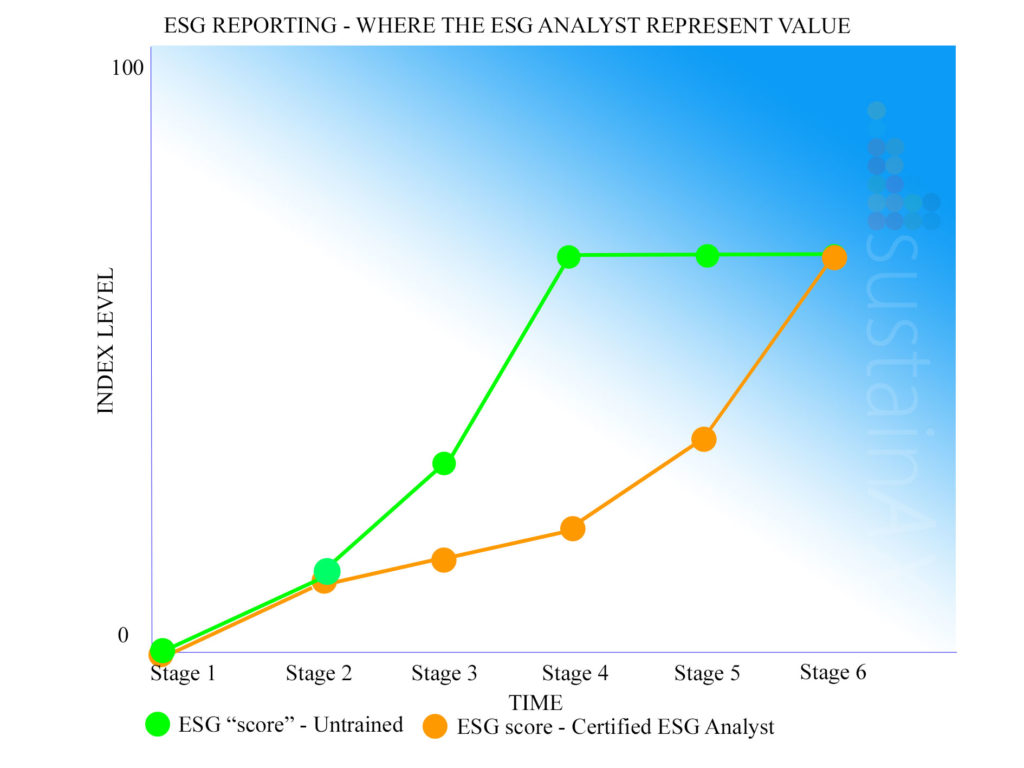

The map and the landscape aspect of sustainability reporting – ESG scores

Today, a «good» ESG profile of a company can mean lower financing costs, normal as the ESG risk is lower than for comparable companies with «less good» ESG profiles. Getting a good ESG score means money. But as seen in the examples above there are times where the sustainability reporting may not give the correct image of the company as trained ESG specialists can see. But most investors are not trained in real ESG research and will maybe never fully be? When not being a specialist it is normal to presume that the map perfectly reflects the landscape. As ESG analysts, it is our job to see the differences.

The following graph is based on the information in graph 1.

GRAPH 2 – ESG scores tries to track the landscape, not the map!

Source: sustainAX, November 2021

Is regulation helping or impeding progress on sustainability strategy implementation?

Today all push for more sustainability reporting and for the “wrong” reason, regulation. We would prefer the same push for implementing of solid sustainability strategies instead, with following sustainability reporting. In Europe we see SFDR, EU Taxonomy and CSRD regulation leading to a reporting frenzy among investors and companies. Complicated regulation with short deadlines. Unfortunately, it will take resources away from the real development of sustainability strategy development in the coming years.

This is also a resource question, as large companies easier can progress on both at the same time, while companies with less resources will maybe focus on the reporting as this is not a choice, but a legal requirement. It should be said that the extended deadline to 2026 for SMEs’ implementation of CSRD help though.

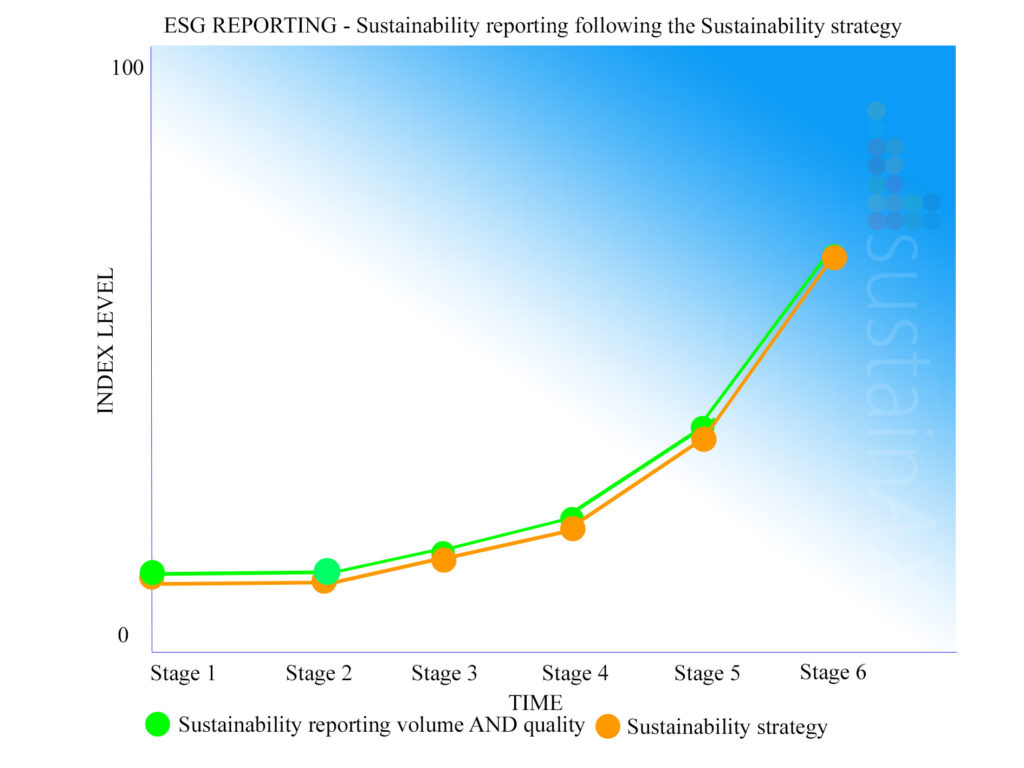

Recommendation to the corporates – Show us hard facts – Action and KPIs

We suggest that the companies should strive to diminish the gaps in the stadium 3 to 5 in the above examples. As ESG analysts, we prefer to see that the sustainability strategy is leading on the sustainability reporting and not the opposite. Maybe hiring a sustainability strategy consultant before or at least at the same time as a CSR/sustainability reporting consultant is an idea? We see reports that could have been cut to half the volume of narratives and instead have been strengthened with KPIs.

The following graph is based on the information in graph 1.

GRAPH 3 – How it could look when sustainability strategy implementation leads

Source: sustainAX, November 2021

It is not for nothing that many ESG specialists prefer to see the sustainability governance attached to the operational top management in a role that is not attached to the communication department. The latter sends a signal about potential wrong priorities or worse, lacking understanding of the importance of a sustainability strategy.

The sustainability strategy is about the long-term survival of the company.

Only when there is a solid sustainability strategy implemented it is possible to explain action supported with good KPIs as these already exist as real internal management steering tools.

What do you think? If you disagree, we are interested to hear it and maybe you can help us understand better! Maybe you recognise the stadium where your company is today?