ESG* Reporting – How to split the “responsibility” of CO2 emissions for those financing a company – A suggestion for the banks and asset managers

Most banks state that their biggest impact on the environment is through the financing they do of other companies. But they are not the only source of financing of the activity. There are also shareholders and bond investors, most of these in terms of volume are asset managers. The remaining part of the financing of the activity is supplier debt, etc. All sums up to the passive side of the balance sheet of the company.

It is hard to estimate the Scope 3 today, as a lot of companies do not publish data, it is too scattered among a multitude of clients, and there is no agreement how to measure all correctly.

Some banks and asset managers do an effort of estimating it, with the risk of being wrong. But really, it is to their advantage to try to put a number on it, and we recommend doing so. It makes all words about sustainability and contribution to common environmental and societal goals, like the UN SDGs, carry more weight.

Then the question is how to do this?

Some banks do this with a rough approach today, for instance you can look at each industry’s CO2 emissions, their total debt and then take your part of debt per industry and hence deduce your “financing” of CO2 emissions.

The weakness to this approach is that banks take all the “responsibility” for the CO2 emissions.

This is the same for shareholders and bond holders were they to estimate just their Scope 3 based on the % of their specific asset class of the company in question.

The result is that they all come up with a far too high Scope 3 number, where the sum of them all is 3 times bigger than the real emissions of the financed activity.

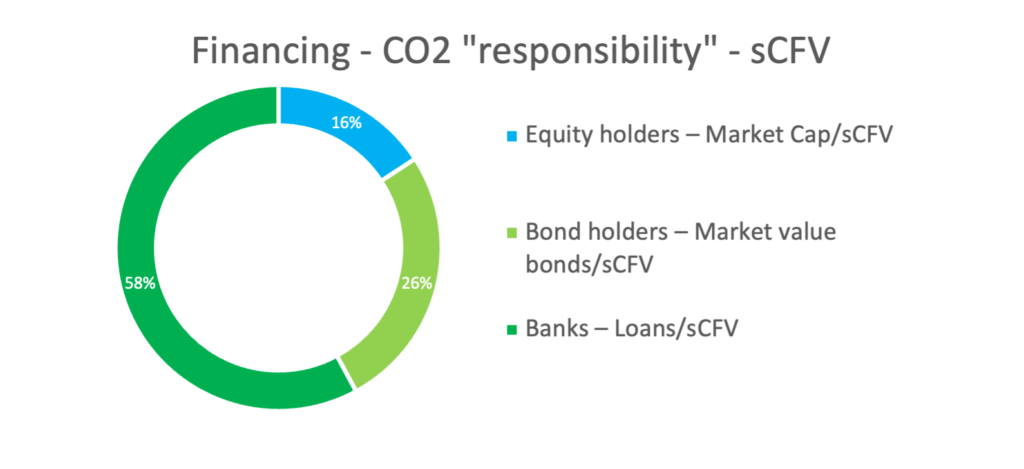

CO2 Scope 3 – Share the CO2 “responsibility” by splitting per % of sCFV

sustainAX definition of sCFV (sustainAX Carbon Financing Value):

sCFV = Equity Market Cap + Market Value Bonds + Bank Loans

How to share the % “responsibility” of the CO2 emissions:

- Equity holders – Market Cap/sCFV

- Bondholders – Market value bonds/sCFV

- Banks – Loans/sCFV

Figure 1 – CO2 emission “responsibility” of different sources of financing based on sCFV (sustainAX Carbon Financing Value)

source: sustainAX

It will be more correct as it reduces double counting of the CO2 emissions.

With this approach all banks and fund managers can do accounting of their “share” of the CO2 emissions of the activities they finance and hence report on the financing Scope 3. For asset managers, this could be specified per fund and the asset owners (those investing in funds) could with their % ownership in a fund repost on their own Scope 3.

The missing part would be the rest of the passive side of the balance sheet financing element, that is supplier debt, etc.

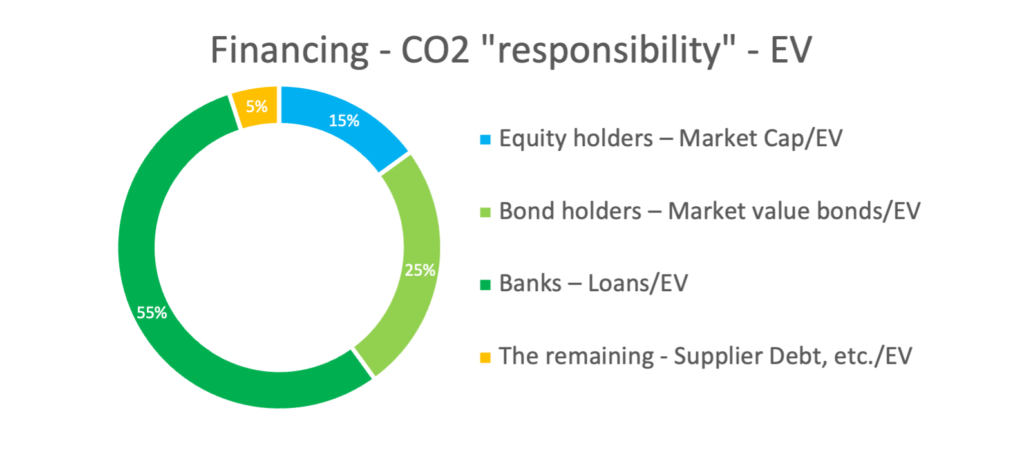

An approximate way of approaching this is to relate the different financing sources to the Enterprise Value (EV)

Here also, the missing part in reality would be the rest of the passive side of the balance sheet financing element, that is supplier debt, etc. But as in EV the cash should be deducted, we can in the big picture ignore this element.

How to share the % “responsibility” of the CO2 emissions based on EV:

- Equity holders – Market Cap/EV

- Bondholders –Bonds Debt/EV

- Banks – Loans/EV

- The remaining – Supplier Debt, etc. minus Cash

Figure 2 – CO2 emission “responsibility” of different sources of financing based on sCFV (sustainAX Carbon Financing Value)

source: sustainAX

For both approaches, there will always be some cases where this gives wrong results, but in a portfolio approach these effects will normally be very diluted.

What do you think about this?