Regulation – How too many misunderstand SFDR and what that leads to – How to address!

EU’s Sustainable Finance currently has one main topic, that is to reduce GHG emissions as a step in reaching the 2050 goals with lower global temperature increases.

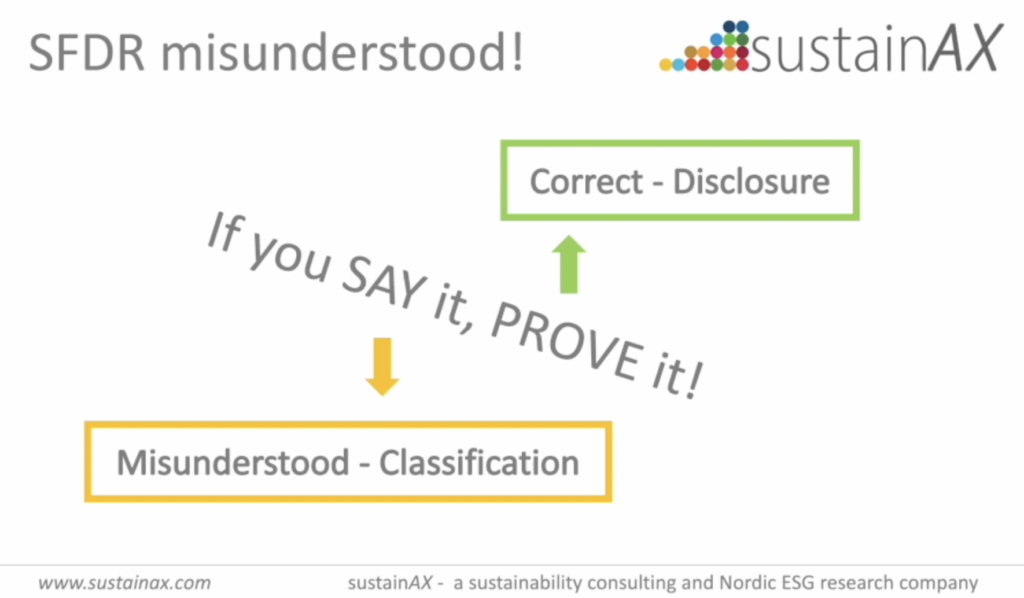

As a part of the EU Sustainable Finance, EU has introduced the SFDR (Sustainable Finance Disclosure Regulation). Notice well the word “Disclosure” and keep it alive as you read the following. EU’s target is to ensure information relevant to Sustainable Finance is disclosed for financial products. This is a regulation that has as main target to increase transparency for investors, so that greenwashing* (and socialwashing*) optimally disappears or at least diminish. We could simplify the whole SFDR to “If you say it, prove it!”

For many today, the above points have vanished somewhere in the background, and they have misunderstood and are misusing this regulation. This leads to a lot of quasi debates, opinions and questions that are irrelevant and a waste of time.

What do we hear today? “The Art 8 funds are greenwashing!”, “The SFDR classification is not aligned with Sustainable Finance”, etc. All expressions showing misunderstanding. A lot is circulating around the Art 8. But we also hear “this is an Art 6 fund”, and what does this really mean?

How come SDFR was misunderstood? Focus on “If you SAY it,…”

As a starting point, the asset managers did not want this, they preferred to self-regulate as finance always does. And when the regulation was shaping, most asset managers were looking for quick fixes, any would do. Unfortunately, many are still there. Many opinions, but few has really read and worked directly with this regulation. Many base their opinions on headlines and consultant summaries.

As this regulation came along, it was perceived that not being regulated by an SFDR Article with a high “enough” number (among Art 6, 8 and 9) was a commercial catastrophe. Here the sales departments took control of the process and quickly the SFDR was misused as a classification regulation. This spread into many departments in asset managers and today specialists have often given up and align, the steamboat is too heavy to turn around. I take the fight; it is important that SFDR is fully understood to avoid misuse.

What does the misunderstanding of SFDR lead to?

SFDR Art 6

We see many refer to funds not being regulated by Art 8 or 9 as “Art 6 funds”, like it meant “all other” funds. This makes no sense, is wrong and only lack of knowledge or insight can lead to this use. This takes attention away from the very important content of this article, that is the information whether ESG risks are integrated or not. PLUS, for the first how, and for the second why!

SFDR Art 8

Well, if you think this is a classification regulation, there is no wonder why so many thought that exclusions without minimum thresholds should not be enough to “qualify” for Art 8 “classification”. Many read elements into the regulation that were not written. Unfortunately, the ESAs called the funds regulated by Art 8 “light green” a bad choice as this strengthens the misuse. The answers from the EU in the summer 2021 were crystal clear! This is not about thresholds, but about information requirements according to what you say the fund is offering (what is “promoted”).

For all the above, when misused as described, the focus is on the commercial side (Look! It has an Art 8 “label”!), while we recommend the asset managers to focus on the information side in line with the SFDR. The latter will also reveal the very important requirement of real action, that is the real processes behind. We see many woolly SFDR texts on websites and in prospectuses. We wonder how well the processes behind are really working and here we have a particular worry for Art 6, where most investors of actively managed funds claim they integrate ESG risk. We think there is a lot of work left to be done here and that when the FSAs start to monitor and control this it can be painful.

How SFDR should be used? Focus on “…PROVE it!”

As mentioned in the beginning of this article, this is a “Disclosure” regulation and should be understood and used like that. Do not use this as a labelling regulation and you will see that a lot of time and energy is spent on unnecessary debates.

Examples

- Instead of saying “this is classified as an Art 6 fund” start saying, “the fund integrates ESG risks in the investment decisions (or not) regulated by Art 6”.

- Instead of saying “this is classified as an Art 8 fund” start saying “this is a fund that promotes environmental and/or social characteristics regulated by Art 8” or at least make it clear that this is what is meant. The latter is a more likely way forward as these expressions have grown deep.

The funds being regulated by Art 8 is a very large and varied group, and EU is aware of and expected this. They probably count on investors and asset owners to use the better information to divest the funds with the lightest promoted binding characteristic to redeploy the assets in funds with heavier characteristics and this way steer the capital towards funds with more environmental and social characteristics. Maybe even jumping to Sustainable Investments that is regulated by Art 9. There is an element of “shame” but also responsibility that EU counts on here. Will it work? We will see, but likely.

SFDR savviness – Utopia?

Most will think that this article is an overload in semantics, and I can see that. It is so convenient to use “Art 6, Art 8 and Art 9” when talking about these funds. Fine, but it has led to a lot of misunderstanding already, time to clean up!

My main point is that in discussions, inhouse or externally with clients and peers, be precise and ensure that you understand the SFDR regulation’s point. Start the topic in meetings with a reminder that this is a reporting regulation and not a classification or labelling regulation. Continue saying that the regulation is about ensuring that you as an asset manager can prove with pertinent information that you do what you claim for the products. Then focus on the processes, explain how they work to show you deliver what you are promising.

Recommendations – How to use the SFDR right?

Now I really wonder how many got this far in this article, those that did will be stronger in the “ESG” competitive race.

I recommend all to read the SDFR Level 1 regulation text, it is not that long, and it will make you see what is discussed here today. It will cost you a couple of hours. Be good at this, this regulation is transforming the asset management industry, but not all have seen this yet. Why? Because they have not always taken the time to study this close enough.

*Greenwashing (Social-) – Faulty claiming a financial product has an environmental (social) characteristic or contributes to an environmental (social) goal